Sharp Decline in Southeast Asian Plastic Resin Prices Raises Industry Concerns

The Southeast Asian plastic resin market has experienced significant price reductions across most major product lines this week, raising questions about whether this represents a short-term adjustment or signals the beginning of a new downward cycle for the industry. With many manufacturers now forced to scale back production, the current market downturn presents both challenges and potential opportunities for stakeholders.

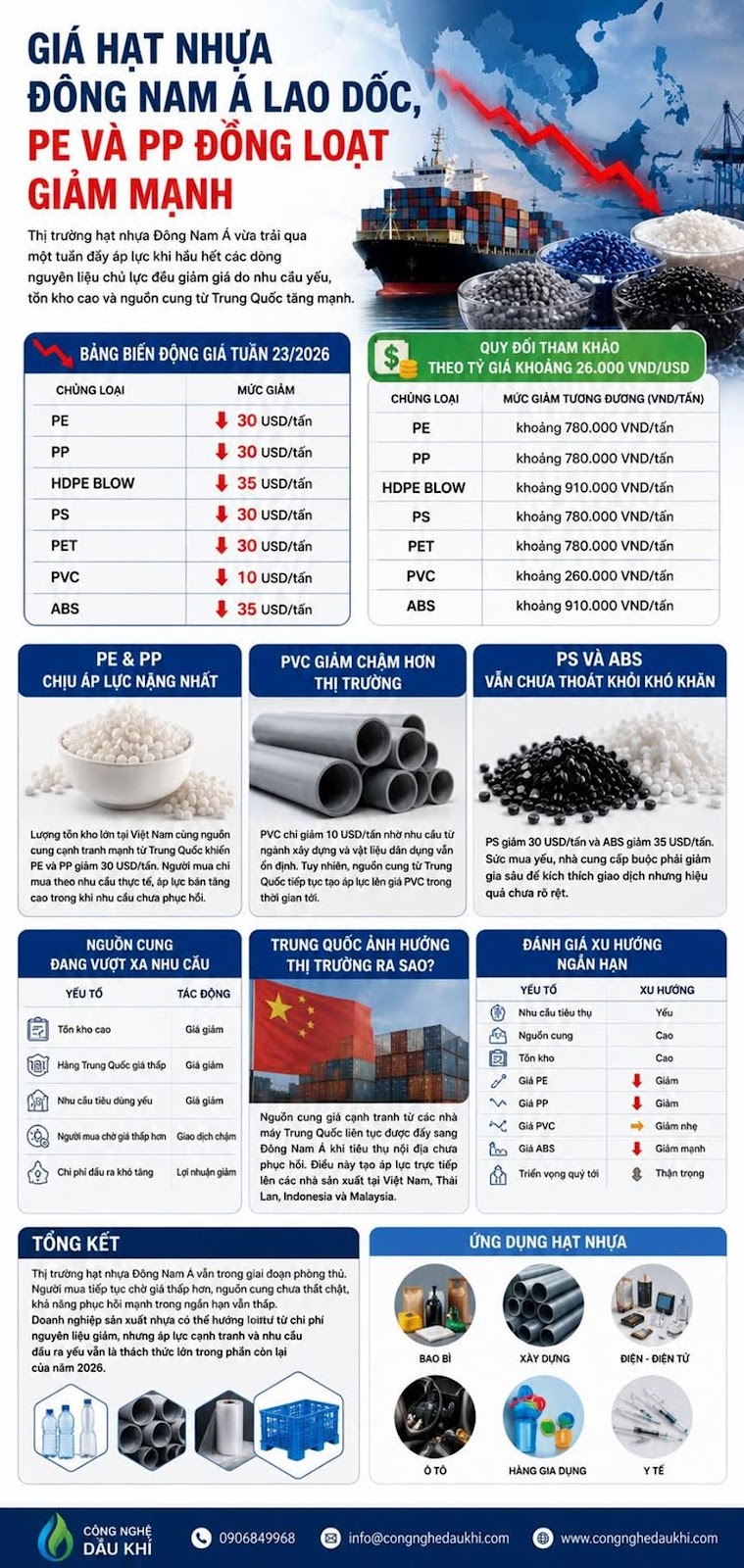

Comprehensive Price Analysis for Week 23, 2026

The market has witnessed unprecedented price reductions across virtually all plastic resin categories. The following table details the magnitude of these decreases:

| Resin Type | Price Reduction (USD/ton) |

|---|---|

| PE (Polyethylene) | -30 USD |

| PP (Polypropylene) | -30 USD |

| HDPE Blow | -35 USD |

| PS (Polystyrene) | -30 USD |

| PET (Polyethylene Terephthalate) | -30 USD |

| PVC (Polyvinyl Chloride) | -10 USD |

| ABS (Acrylonitrile Butadiene Styrene) | -35 USD |

Based on an approximate exchange rate of 26,000 VND/USD, these price reductions translate to the following decreases in Vietnamese currency:

| Resin Type | Price Reduction (VND/ton) |

|---|---|

| PE | Approximately 780,000 VND |

| PP | Approximately 780,000 VND |

| HDPE Blow | Approximately 910,000 VND |

| PS | Approximately 780,000 VND |

| PET | Approximately 780,000 VND |

| PVC | Approximately 260,000 VND |

| ABS | Approximately 910,000 VND |

PE and PP Markets Under Maximum Pressure

Polyethylene (PE) and Polypropylene (PP) continue to bear the brunt of the price decline in the regional market. These fundamental resin types are experiencing the most severe downward pressure due to a combination of factors:

- Large inventory buildup in Vietnam and other Southeast Asian countries

- Aggressive competition from Chinese suppliers offering lower-priced alternatives

- Shift in purchasing behavior from inventory stocking to order-based procurement

Manufacturers of packaging, consumer plastic goods, and industrial plastics have significantly altered their procurement strategies, moving away from previous inventory accumulation practices. This change in purchasing behavior has intensified selling pressure while demand has failed to recover proportionally.

Supply-Demand Imbalance Analysis

The current market situation is characterized by a significant supply-demand imbalance, as illustrated in the following table:

| Market Factor | Impact on Market |

|---|---|

| High Inventory Levels | Price Reduction |

| Low-Priced Chinese Imports | Price Reduction |

| Weak Consumer Demand | Price Reduction |

| Buyers Waiting for Lower Prices | Slowed Transaction Volume |

| Inability to Increase Output Costs | Reduced Profit Margins |

PVC Market Shows More Resilience

Notably, Polyvinyl Chloride (PVC) has demonstrated relative resilience with a price reduction of only approximately 10 USD/ton—significantly less than PE and PP. This relative stability can be attributed to:

- Consistent demand from the construction and civil materials sectors

- More stable transaction volumes compared to other resin types

- Government infrastructure projects maintaining baseline demand

However, the persistent pressure from Chinese supply sources suggests that PVC prices may face additional challenges in the coming months despite current relative stability.

PS and ABS Continue to Face Significant Challenges

Polystyrene (PS) and Acrylonitrile Butadiene Styrene (ABS) continue to experience negative market performance. These engineering plastics face particularly challenging conditions:

- Manufacturers of consumer goods, electronic components, and technical plastics maintain cautious purchasing attitudes

- Suppliers have implemented deep price cuts to stimulate transactions with limited success

- ABS has emerged as one of the most severely impacted resins, matching HDPE Blow with a 35 USD/ton price reduction

The persistent weakness in these high-value resin segments reflects broader economic challenges affecting downstream manufacturing sectors, particularly in electronics and consumer durables.

China's Growing Influence on Regional Markets

China has emerged as the most significant factor affecting regional plastic resin prices. The Chinese market's impact manifests in several key ways:

- Continuous flow of competitively-priced resin from Chinese manufacturers into Southeast Asia

- Weak domestic consumption in China driving export-oriented sales strategies

- Direct competitive pressure on producers in Vietnam, Thailand, Indonesia, and Malaysia

- Price-setting influence that dominates regional market dynamics

This Chinese influence has fundamentally altered the competitive landscape, forcing regional producers to either match Chinese prices or differentiate through quality and service offerings.

Short-Term Market Outlook Assessment

The following table summarizes key market factors and their likely impact on short-term trends:

| Market Factor | Expected Trend |

|---|---|

| Consumer Demand | Weak |

| Supply Availability | High |

| Inventory Levels | Elevated |

| PE Prices | Declining |

| PP Prices | Declining |

| PVC Prices | Mild Decline |

| ABS Prices | Sharp Decline |

| Q3 2026 Outlook | Cautious |

Market Implications and Strategic Considerations

Overall, the Southeast Asian plastic resin market remains in a defensive posture. As buyers continue to anticipate lower prices and supply shows no signs of tightening, the potential for a strong recovery in the short term remains limited. While plastic manufacturers may benefit from reduced raw material costs, the challenges of intensified competition and weak output demand present significant obstacles for the remainder of 2026.

Industry participants should consider several strategic responses to this challenging market environment:

- Inventory optimization to minimize carrying costs while maintaining operational flexibility

- Product differentiation strategies to move beyond commodity pricing competition

- Cost structure review to identify potential efficiency improvements

- Market diversification to reduce dependence on price-sensitive segments

- Long-term supply chain restructuring to mitigate China's market influence

The current market downturn, while challenging, may also present opportunities for consolidation and strategic positioning among stronger market participants who can navigate this difficult period effectively.